Umbrella insurance for rental property owners is a crucial safety net that extends beyond typical landlord insurance, providing an extra layer of protection against unforeseen liabilities. As a rental property owner, you’re not just managing properties but also facing potential financial risks that can arise unexpectedly from accidents or damages. Understanding how this additional coverage works can empower you to safeguard your investments effectively.

This type of insurance is designed to cover claims that exceed the limits of your standard insurance policies, ensuring that you’re not left vulnerable in the event of a significant incident. From protecting your assets against lawsuits to covering damages that might occur on your property, umbrella insurance plays a vital role in risk management for property owners.

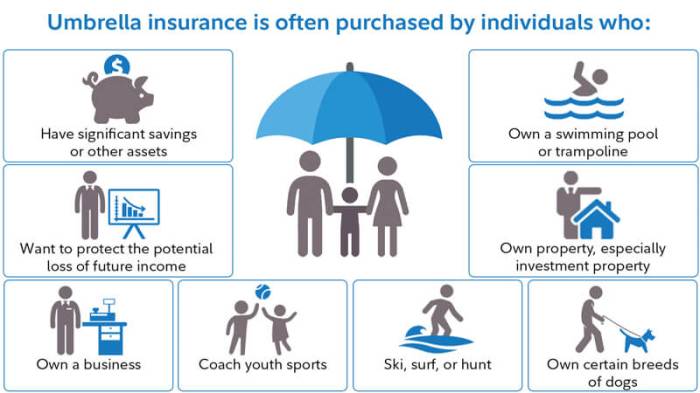

Understanding Umbrella Insurance for Rental Property Owners

Rental property owners face unique challenges and risks that extend beyond standard landlord insurance policies. Umbrella insurance serves as an additional layer of protection, safeguarding owners against significant financial losses from unforeseen events. This type of insurance is particularly crucial for those who manage multiple properties or have substantial personal assets at stake.Umbrella insurance is designed to provide coverage that goes above and beyond the limits of standard liability coverage included in landlord insurance policies.

This means that if a claim exceeds the limits of the underlying insurance, umbrella insurance can kick in to cover the additional costs. It serves not just as a safety net, but as a financial shield against potential lawsuits and claims that could drain your resources.

Coverage Options Provided by Umbrella Insurance

Umbrella insurance offers a broad range of coverage options that can significantly benefit rental property owners. Its extended coverage includes, but is not limited to, the following:

Liability Coverage

This covers legal costs and damages if a tenant or visitor is injured on your property and decides to sue.

Personal Injury Claims

Claims related to defamation, invasion of privacy, or false arrest can be covered under umbrella insurance, which is often not included in standard policies.

Damage to Property

If a rental property damage claim exceeds the limits of your primary insurance policy, umbrella insurance can cover the excess amount.

Legal Defense Costs

Legal fees can accumulate quickly. Umbrella insurance may cover these costs even if the claims against you are found to be groundless.By providing such comprehensive coverage, umbrella insurance helps mitigate the financial risks that rental property owners may encounter.

“Umbrella insurance safeguards your finances by covering unexpected legal liabilities that could arise from your rental properties.”

The potential financial risks that can be mitigated through the use of umbrella insurance include catastrophic events such as severe accidents, natural disasters leading to tenant disputes, and high-stakes lawsuits. Rental property owners are inherently exposed to these risks due to the nature of their business, making umbrella insurance a wise investment for anyone seeking to protect their assets and ensure peace of mind.

Comparison of Different Types of Insurance for Property Owners

Choosing the right insurance for rental property can be a daunting task, especially with the variety of options available. Understanding how different types of insurance work together allows property owners to better protect their investments and mitigate risks. This comparison covers umbrella insurance, pet insurance, supplemental insurance, and travel insurance, highlighting their relevance and use in the context of rental property ownership.

Umbrella Insurance and Pet Insurance

Umbrella insurance provides an extra layer of liability coverage above and beyond existing policies. For property owners with pets, pet insurance can play a significant role in managing risk. While umbrella insurance protects against liability claims that exceed standard coverage limits, pet insurance specifically covers veterinary expenses related to injuries or illnesses incurred by the pet.The connection between the two types of insurance is crucial for property owners.

If a tenant’s pet causes damage or injury, the property owner’s umbrella policy can cover the resulting liability, while pet insurance can cover the pet’s own medical issues. This holistic approach ensures that both the property and the pet’s health are safeguarded.

Supplemental Insurance and Its Role

Supplemental insurance serves as an additional protective measure that complements existing policies, including umbrella insurance. It can cover gaps in standard rental property insurance, offering expanded coverage for specific risks that may not be addressed in the primary policy. Property owners should consider the following benefits of supplemental insurance:

- Higher liability limits for specific scenarios, such as natural disasters or tenant actions.

- Coverage for specific incidents like vandalism or theft that might not be fully covered by standard policies.

- Protection for personal property within the rental unit, enhancing overall security.

Supplemental insurance can work hand-in-hand with umbrella insurance to provide comprehensive protection tailored to the unique risks associated with rental properties.

Travel Insurance for Frequent Travelers

Travel insurance is particularly relevant for property owners who travel frequently. When owners are away, the risk of unforeseen events impacting their rental properties, such as damage or liability claims, increases. Travel insurance can protect property owners from financial losses incurred during their travels, ensuring continued peace of mind.Some crucial aspects of travel insurance for property owners include:

- Emergency assistance for renters or property managers in case of emergencies while the owner is away.

- Coverage for trip cancellations, allowing property owners to recoup costs if they need to change their travel plans.

- Protection against loss or damage to personal belongings while traveling, which can indirectly impact rental operations.

By integrating travel insurance with existing coverage, property owners can create a robust safety net that allows them to manage their properties effectively, even while away.

Comprehensive Guide to Various Insurance Types

Understanding the different types of insurance available is crucial for rental property owners. Each type of insurance serves a unique purpose and offers specific protections, which can help mitigate risks associated with property management. This guide aims to clarify some key insurance options, focusing on vision insurance, watercraft insurance, and a comparison of umbrella insurance with other types of insurance.

Vision Insurance Features for Property Owners

Vision insurance is an important consideration for property owners, as maintaining good health is vital for effective property management. Key features to consider in vision insurance include:

- Coverage for Eye Exams: Regular eye examinations can help identify vision problems early, thereby enhancing productivity and safety in property management tasks.

- Prescription Eyewear Discounts: Many policies offer discounts on glasses and contact lenses, ensuring affordable options for clear vision.

- Preventive Care Benefits: Coverage often includes preventive services, which can save property owners from more costly treatments down the line.

- Network of Providers: Access to a broad network of optometrists and ophthalmologists can enhance convenience and choice.

Watercraft Insurance for Rental Property Owners

For rental property owners who provide water-related activities, watercraft insurance is essential. This type of insurance protects against liabilities and damages that may arise from operating boats or other watercraft. Important aspects include:

- Liability Coverage: This covers bodily injury and property damage claims resulting from watercraft accidents, protecting owners from financial losses.

- Physical Damage Coverage: Protects against damages to the watercraft itself from accidents, theft, or vandalism.

- Medical Payments: Provides coverage for medical expenses incurred by passengers injured while using the watercraft.

- Uninsured/Underinsured Boater Coverage: Protects against losses if an accident is caused by a watercraft operator who lacks sufficient insurance.

Comparison of Umbrella Insurance with Other Insurance Types

To better understand the value of umbrella insurance in relation to other policies like pet insurance and supplemental health insurance, a comparison can be helpful. The table below highlights key benefits and coverage limits:

| Insurance Type | Benefits | Coverage Limits |

|---|---|---|

| Umbrella Insurance | Provides additional liability coverage beyond standard policies. | Typically $1 million or more, depending on the policy. |

| Pet Insurance | Covers veterinary costs for pets, including accidents and illnesses. | Varies widely, usually $5,000 to $20,000 per year. |

| Supplemental Health Insurance | Covers out-of-pocket costs not covered by primary health insurance. | Varies based on the plan, with some offering up to $100,000 in coverage. |

Closing Summary

In summary, umbrella insurance serves as a comprehensive solution for rental property owners, providing essential coverage that standard policies may not fully address. By investing in this additional protection, you can confidently manage your rental properties, knowing that you have a safety net in place. Whether you’re facing claims from tenants or unforeseen damages, umbrella insurance helps you navigate the complexities of property management with peace of mind.

FAQ Corner

What is umbrella insurance?

Umbrella insurance is additional liability coverage that goes beyond the limits of your existing insurance policies, offering extra protection for serious claims.

Who should consider umbrella insurance?

Rental property owners, especially those with multiple properties or valuable assets, should consider umbrella insurance to mitigate financial risks.

Does umbrella insurance cover tenant injuries?

Yes, it can cover injuries sustained by tenants on your property, provided the incident exceeds the limits of your landlord insurance.

How much umbrella insurance do I need?

The amount you need depends on your assets, income, and potential risks, but it’s advisable to have at least $1 million in coverage.

Is umbrella insurance expensive?

Generally, umbrella insurance is relatively affordable compared to the level of coverage it provides, making it a cost-effective investment for property owners.